Every second your payment infrastructure is live, fraudsters are probing it. Not metaphorically — literally. Automated bot attacks now execute thousands of synthetic-identity tests per minute against FinTech platforms, and the ones that slip through cost the global payments industry an estimated $44 billion in card fraud losses by 2025, according to McKinsey. Legacy rule-based fraud engines catch the obvious attacks but generate so many false positives that legitimate customers get blocked — killing conversion rates and trust at the same time. The answer isn’t more rules. It’s a fundamentally different architecture: AI fraud detection software that learns continuously, scores transactions in under 50 milliseconds, and achieves accuracy rates above 99% without introducing friction for real customers.

This post is written for CTOs, VPs of Engineering, and Head of Product at FinTech companies who need to understand not just what AI fraud detection does, but how to build or buy it — the architecture decisions, the model tradeoffs, and the ROI you should demand before signing any contract.

Let’s get into it.

What Is AI Fraud Detection Software — and Why It’s Not the Same as Rule-Based Fraud Systems

AI fraud detection software uses machine learning models — trained on historical transaction data, behavioral patterns, device signals, and network graphs — to assign a real-time risk score to every transaction, login, or account action. Unlike static rule-based systems that flag transactions matching predefined criteria (“transaction over $5,000 from a new device”), AI-powered systems identify anomalies in context: they know that a $4,800 transfer from a new device is normal for this specific customer who travels frequently, but flagging a $200 purchase from a device this customer has used for three years but at a merchant category they’ve never transacted with before.

That contextual intelligence is the entire game. And it’s what separates legacy fraud detection from modern AI-powered systems.

Rule-Based Systems: Fast to Build, Slow to Adapt

Rule-based fraud detection was the industry standard for decades. Your fraud team would define logical conditions — velocity rules, geography rules, amount thresholds — and any transaction matching those conditions gets flagged or blocked. The appeal is obvious: it’s transparent, auditable, and relatively simple to implement. The problem is equally obvious: fraudsters read the same playbooks your rule writers do, and they adapt in days. Rule-based systems require months of analyst time to update, and every new rule you add increases the false-positive rate.

According to PwC’s fraud and economic crime research, traditional rule-based transaction-monitoring systems generate false-positive rates between 90% and 95% — meaning the vast majority of alerts your team reviews are legitimate. That’s not a fraud problem; it’s an operations problem that happens to cost more than the fraud itself.

AI-Powered Systems: Adaptive, Contextual, Always-On

AI fraud detection systems operate on a fundamentally different principle. Instead of matching transactions against a predefined list of bad patterns, they build a probabilistic model of what “normal” looks like — for your entire user base, for individual customer segments, and for each individual user — and score every new event against that baseline. The models retrain continuously as new data arrives, which means they adapt to emerging fraud patterns automatically, often within hours rather than months.

The three core capabilities that define enterprise-grade AI fraud detection software are: real-time scoring (sub-100ms decisions at scale), multi-signal fusion (combining transactional, behavioral, device, and network data), and adaptive learning (continuous model retraining without manual rule updates). We’ll break down the architecture behind each of these in the section on core capabilities below.

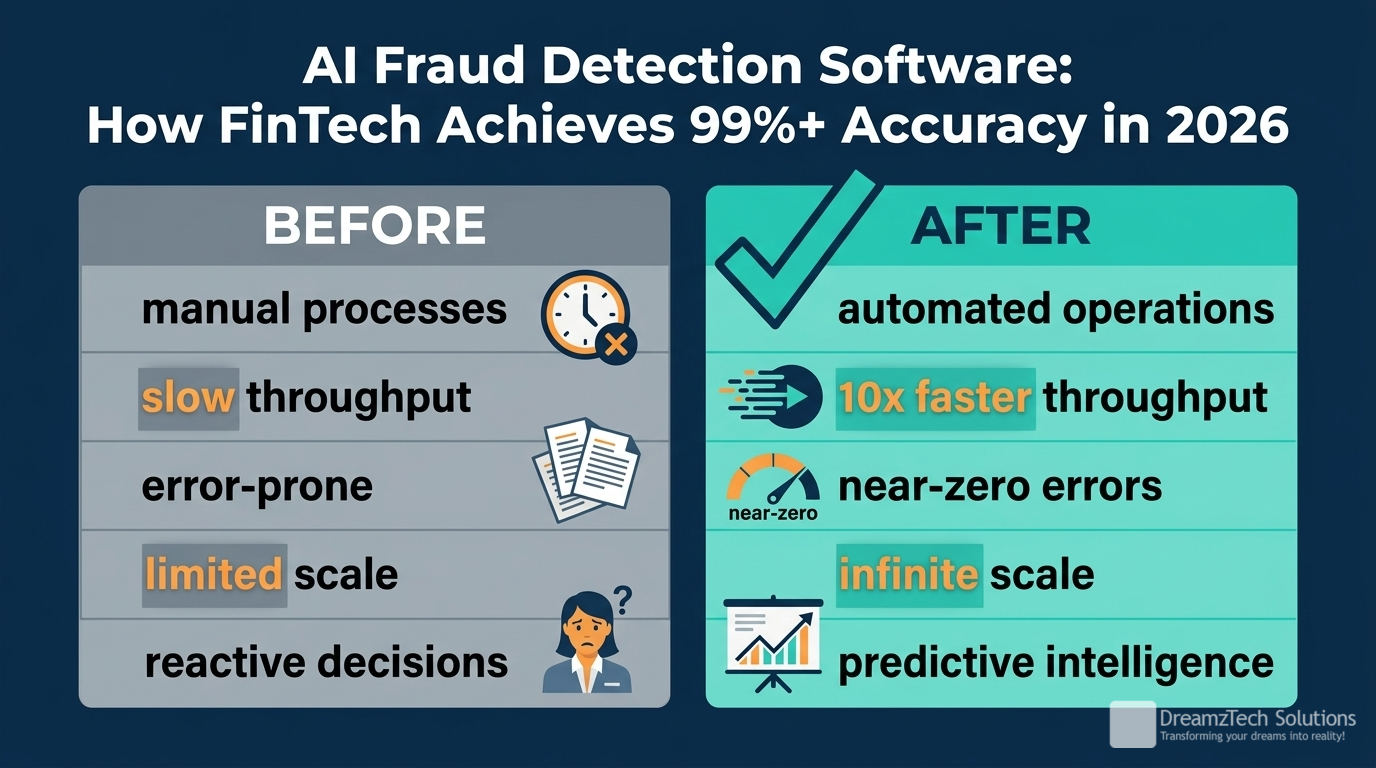

Figure 1: Before and after comparison for AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026

Why 2026 Is the Inflection Point for AI-Powered Fraud Prevention

The fraud landscape has shifted dramatically in the past 24 months — not incrementally, but structurally. Three forces are converging to make legacy detection systems not just insufficient but dangerous to rely on.

The Rise of AI-Generated Fraud

The same generative AI tools that power legitimate business productivity are now weaponized by fraud networks. Synthetic identity fraud — where fraudsters combine real and fabricated personal data to create fictitious identities that pass KYC checks — surged 311% in North America between Q1 2024 and Q1 2025, according to Sumsub’s fraud research. Deepfake audio and video now pass biometric voice verification checks. Large language models generate phishing communications indistinguishable from legitimate bank correspondence. The attack surface is no longer just transactional data — it’s the entire identity verification stack.

Instant Payment Rails Eliminate the Review Window

The global rollout of instant payment infrastructure — FedNow in the US, Faster Payments in the UK, UPI in India, PIX in Brazil — has eliminated the 24-48 hour settlement window that fraud teams historically used to review suspicious transactions before funds moved. When a payment settles in under 10 seconds, your fraud decision has to be made in under 5. There’s no human in the loop for individual transactions at scale. AI is the only viable architecture for real-time decisioning at the volume modern FinTechs operate.

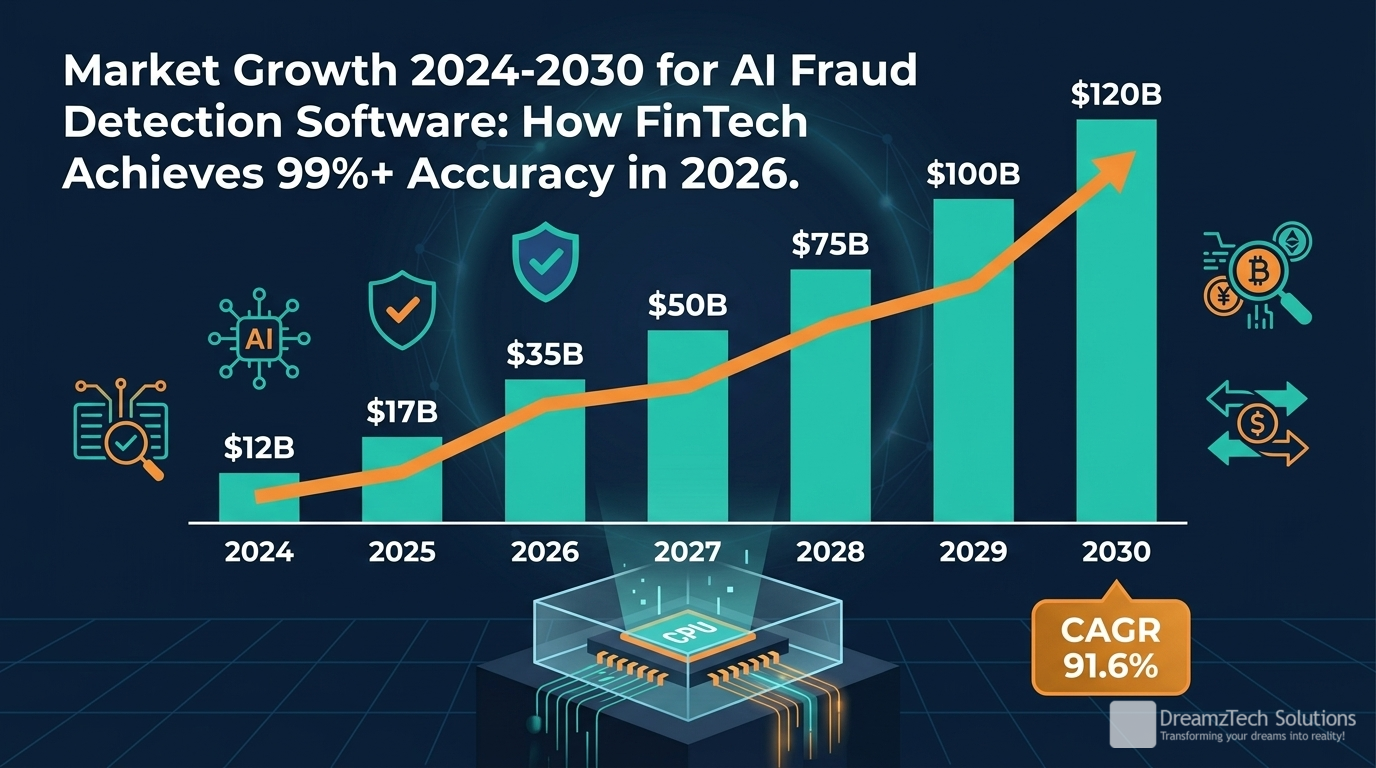

Market Growth Confirms the Shift

The AI fraud detection market reflects this urgency. Grand View Research projects the global fraud detection and prevention market to reach $90.07 billion by 2030, growing at a CAGR of 17.6% from 2023. That’s not a technology trend — that’s a financial services industry recognizing it has no choice. The companies building AI-native fraud infrastructure now will be structurally advantaged over those that wait for a major breach to force the migration.

Figure 2: AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026 market growth 2024-2030

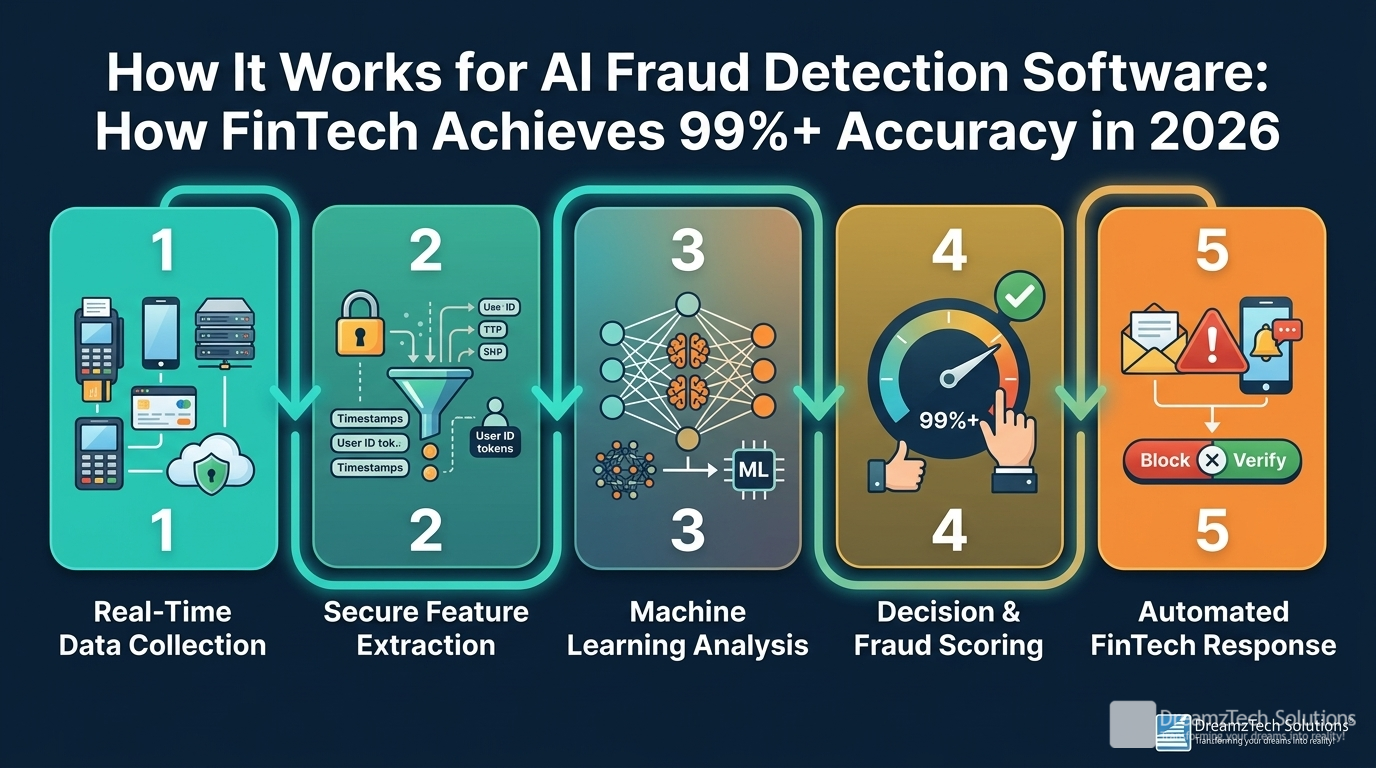

The Architecture Behind 99%+ Accuracy: How Enterprise AI Fraud Detection Actually Works

This is where most vendor pitches stop at buzzwords. We’re going further. Understanding the architectural decisions that drive accuracy, latency, and adaptability will help you evaluate any AI fraud detection solution — whether you’re buying a vendor platform, building in-house, or doing both. At DreamzTech, this is the architecture we implement for clients across the payments, lending, and digital banking verticals.

Layer 1: Real-Time Feature Engineering at the Edge

The foundation of any fraud model is the features it operates on. Garbage in, garbage out — and in fraud detection, “garbage in” means missing the signals that distinguish a fraudster from a legitimate customer at the moment of transaction. Enterprise AI fraud systems ingest signals from at least four categories simultaneously:

- Transaction signals: Amount, merchant category, currency, channel (mobile/web/API), time of day, device used, IP geolocation, shipping address vs. billing address delta

- Behavioral biometrics: Typing cadence, mouse movement patterns, scroll behavior, session duration, click patterns — all captured client-side and compared against the user’s established behavioral baseline

- Device intelligence: Device fingerprint, OS version, browser/app version, jailbreak/root detection, emulator detection, VPN/proxy/Tor detection, SIM swap signals

- Network graph signals: Account-to-account relationships, shared device across multiple accounts, velocity of new account creation from same network, known fraud ring adjacency

The critical architectural point here is that feature computation must happen before the model scores the transaction — and it must happen fast. The best implementations use streaming feature stores (Apache Kafka + Redis for low-latency feature serving) that maintain pre-computed aggregates (rolling velocity counts, user spending averages, device trust scores) so the scoring service never has to compute from scratch. This is how you achieve sub-50ms end-to-end latency while fusing dozens of signals.

Layer 2: The Ensemble Model Stack

No single model architecture achieves 99%+ accuracy across the full spectrum of fraud types. Enterprise-grade AI fraud detection software uses an ensemble — multiple models with different strengths, whose outputs are combined by a meta-learner. A typical production ensemble looks like this:

- Gradient Boosted Trees (XGBoost/LightGBM): The workhorse for tabular transaction data. Excellent at capturing non-linear feature interactions. Produces fast, interpretable scores and handles class imbalance well with proper sample weighting.

- Recurrent Neural Networks / Transformers: Sequence models that capture temporal patterns — the order and timing of transactions matters. A transformer trained on transaction sequences can identify account takeover patterns (sudden velocity change + new payee) that look individually normal but sequentially suspicious.

- Graph Neural Networks (GNNs): The emerging standard for network-based fraud detection. GNNs model the relationships between accounts, devices, and IP addresses as a graph and identify fraud rings — where individually clean-looking accounts are actually part of coordinated synthetic identity networks. AWS publishes reference architecture showing GNNs meaningfully outperforming tabular-only models for fraud ring detection, though the exact lift varies by dataset and fraud type.

- Unsupervised Anomaly Detection: Isolation Forests and Autoencoders that flag statistically anomalous events without needing labeled fraud examples — critical for catching novel fraud patterns that don’t appear in historical training data.

The meta-learner — typically a lightweight logistic regression or a second-stage gradient booster — combines the outputs of these models into a single fraud probability score. Thresholds on this score determine whether a transaction is approved, reviewed, or declined. Calibrating these thresholds is where the real business logic lives: a 0.7 probability score might mean “approve with step-up authentication” in one context and “decline immediately” in another, depending on the transaction type and customer risk tier.

Layer 3: Decision Orchestration and Explainability

A fraud score is not a decision. The decision layer — often called the fraud decisioning engine — applies business rules on top of the model score to produce the final action: approve, decline, step-up auth (OTP, biometric), or queue for human review. This layer handles regulatory requirements (you often must be able to explain a decline to a customer), velocity controls, and exception handling for high-value accounts.

Explainability is non-negotiable in financial services. Regulators in the EU (under the AI Act and GDPR), the US (under ECOA and FCRA), and across APAC require that automated adverse actions be explainable. Modern AI fraud systems use SHAP (SHapley Additive exPlanations) values to generate human-readable explanations for every decision — identifying the top contributing features that drove the fraud score for that specific transaction. This isn’t just regulatory compliance; it’s operationally essential for your fraud analysts to trust and act on the system’s outputs.

Layer 4: Continuous Learning and Model Lifecycle Management

This layer is where most build-vs-buy decisions get made wrong. A fraud model trained on last year’s data will degrade — sometimes sharply — as fraud patterns evolve. Production AI fraud detection requires automated retraining pipelines that ingest newly labeled fraud cases (confirmed by human review queues or chargeback data), retrain models on a cadence (daily or weekly), evaluate the challenger model against the champion on held-out data, and promote the challenger automatically if it meets accuracy and latency thresholds. This is full MLOps — and it requires a mature platform foundation. Building it from scratch is a 6-12 month engineering investment before you write a single model line of code.

Figure 3: How AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026 works step by step

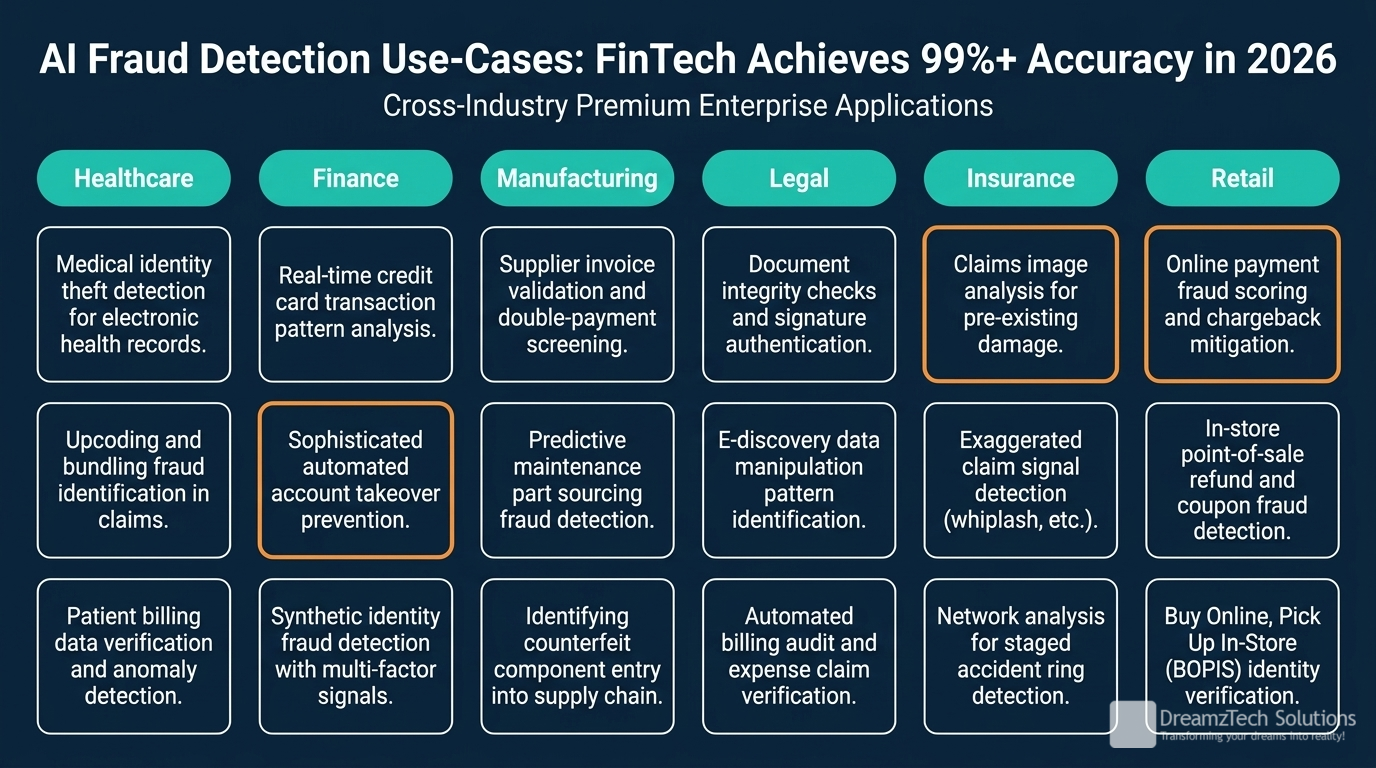

Industry Use Cases: Where AI Fraud Detection Delivers the Biggest ROI

The fraud threat profile varies significantly by FinTech vertical. Understanding where AI-powered detection creates the most value helps you prioritize your implementation roadmap and build the business case for investment.

Digital Payments and Card Issuers

Card-not-present (CNP) fraud — where stolen card details are used for online purchases without the physical card — accounts for the majority of payment card fraud globally. AI models trained on merchant category patterns, transaction velocity, and device fingerprints can reduce CNP fraud rates to under 0.1% of transaction volume while maintaining approval rates above 98% for legitimate customers. The economic case is direct: for a FinTech processing $10 billion in annual payment volume, moving from a 0.4% fraud rate to 0.1% saves $30 million per year — before counting the operational savings from reduced chargeback handling.

Digital Lending and BNPL Platforms

Buy-now-pay-later platforms are prime targets for synthetic identity fraud, where fraudsters build a synthetic credit profile, make small purchases to establish repayment history, then execute a large fraudulent purchase and disappear. AI systems with graph neural network capabilities are particularly effective here — they identify the network signatures of synthetic identity factories even when individual identities appear clean. industry data suggests BNPL platforms using AI-powered identity verification and graph-based network analysis can meaningfully reduce synthetic fraud losses compared to traditional bureau-check-only approaches.

Neobanks and Digital Account Origination

Account opening is the highest-risk moment in the customer lifecycle. Fraudsters invest months in creating believable account profiles specifically to exploit the origination funnel. AI-powered identity verification — combining document authenticity checks, biometric liveness detection, database cross-referencing, and behavioral signals from the onboarding flow itself — can reduce fraudulent account creation by over 80% without increasing friction for legitimate applicants. The key metric: legitimate customers who abandon onboarding due to friction cost as much as fraudsters who get through.

Crypto Exchanges and DeFi Platforms

The pseudonymous nature of blockchain transactions makes crypto platforms uniquely vulnerable — and uniquely suited for graph-based AI fraud detection. Blockchain transaction graph analysis can trace fund flows across wallets, identify mixing services and tumbler patterns, and flag transactions with high exposure to known illicit addresses. industry observers note that crypto platforms investing in AI-powered compliance and transaction-monitoring stacks tend to reduce regulatory penalty exposure, since automated screening flags sanctions and AML violations earlier than manual review alone.

Insurance and Claims Processing

Claims fraud — staged accidents, inflated repair estimates, duplicate claim submissions — costs the global insurance industry an estimated $80 billion annually. AI systems that cross-reference claims data against historical patterns, social network connections between claimants and service providers, and geospatial data can flag suspicious claims at submission, before payouts are made. The ROI on claims fraud AI is often the fastest of any vertical: investigation costs drop immediately, and prevention rates typically exceed 70% within the first six months of deployment.

Figure 4: AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026 industry use cases

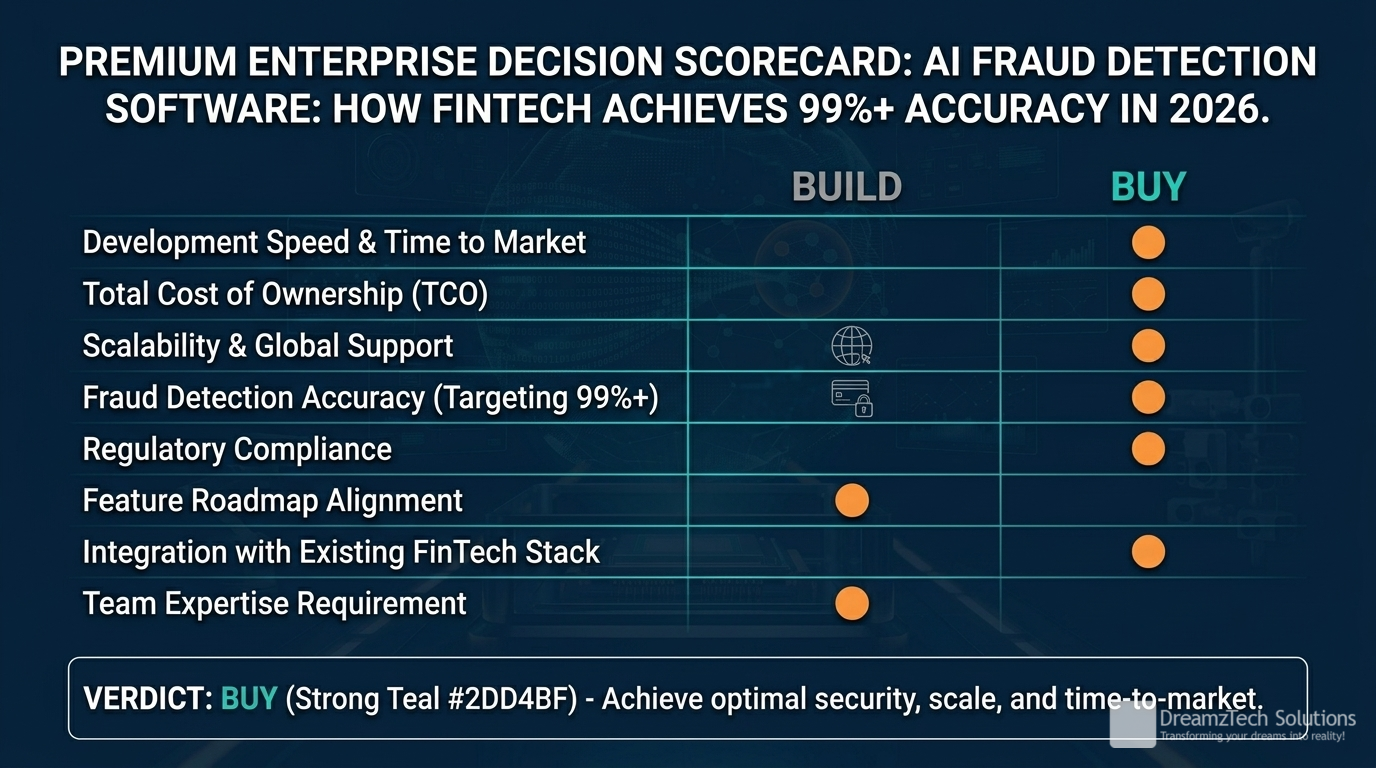

The Buyer’s Checklist: How to Evaluate AI Fraud Detection Software

Whether you’re evaluating a vendor platform, scoping an in-house build, or assessing a hybrid approach, these are the criteria that separate enterprise-grade AI fraud detection from marketing-dressed rule engines. Use this as your RFP framework and due diligence checklist.

Technical Capability Criteria

Start with the architecture questions. Any vendor or engineering team that can’t answer these clearly is not operating at enterprise grade:

- Latency SLA: What is the p99 scoring latency under peak load? Anything above 150ms is a problem for real-time payment decisioning. Ask for load test results, not marketing specs.

- Model architecture: What model types are in the ensemble? A vendor using only rule-based logic with a thin ML layer on top is not the same as a genuine ensemble of gradient boosted trees, sequence models, and GNNs.

- Feature coverage: How many signal categories does the system ingest? Transactional-only systems will miss behavioral and network-based fraud patterns.

- Retraining cadence: How often do models retrain? What triggers a retrain? How long before newly confirmed fraud cases influence live scoring? The answer should be “hours to days,” not “quarterly releases.”

- Explainability: Can the system generate per-decision SHAP explanations? Can those explanations be surfaced to human reviewers and customers in plain language?

- Unsupervised detection: Does the system flag novel fraud patterns it hasn’t seen before, or only patterns matching historical fraud labels?

Operational and Integration Criteria

Technical accuracy means nothing if the system can’t integrate into your infrastructure and your team can’t operate it effectively:

- API design: Is there a clean REST or gRPC decisioning API with documented request/response schemas? What’s the version management policy?

- Case management: Does the platform include a fraud analyst workbench for reviewing flagged transactions, providing feedback labels, and tracking investigation outcomes?

- Cloud compatibility: Does it deploy on your existing cloud infrastructure (AWS, Azure, Google Cloud)? Does it lock you into a proprietary stack?

- Custom model support: Can your data science team bring custom models into the decisioning pipeline? Or is the model stack black-box and vendor-controlled?

Compliance and Regulatory Criteria

Financial services AI carries regulatory obligations that pure technology vendors often underestimate:

- Adverse action explainability: Can the system generate FCRA/ECOA-compliant adverse action notices for declined transactions or applications?

- Bias and fairness testing: Has the model been audited for discriminatory patterns across protected demographic groups? In the US, EU, and UK, biased automated financial decisions create material legal liability.

- Data residency: Where does customer data used for model training and scoring reside? This is critical for GDPR (EU), LGPD (Brazil), and PDPA (APAC) compliance.

- SOC 2 Type II / ISO 27001: Security certifications are table stakes for any vendor handling financial transaction data.

Figure 5: AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026 evaluation scorecard

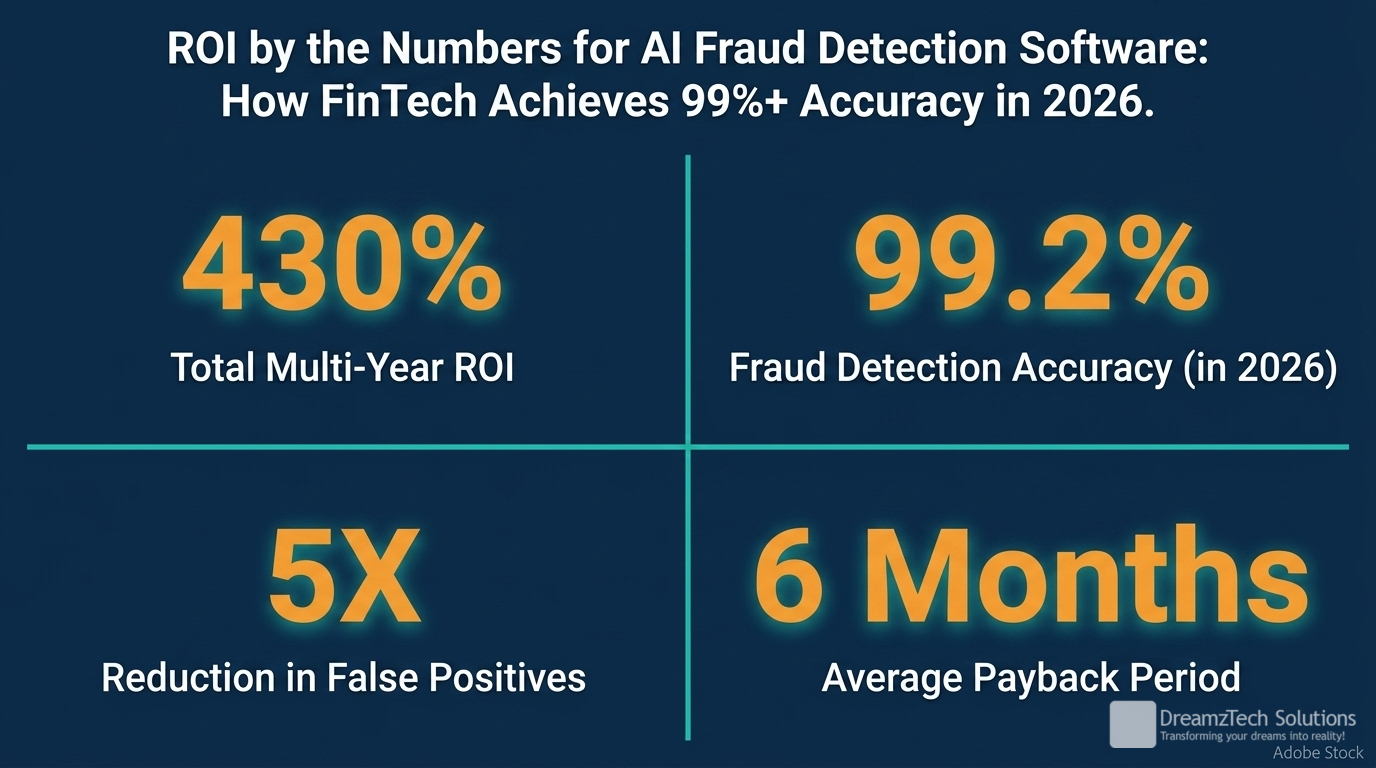

ROI by the Numbers: What the Data Shows

Building the business case for AI fraud detection investment requires concrete numbers. The ROI case is strong — but the specific figures depend on your current fraud rate, transaction volume, and operational baseline. Here’s the data framework we use with clients at DreamzTech, calibrated against published industry research.

Direct Fraud Loss Reduction

The primary value driver is straightforward: AI systems catch more fraud, earlier, with fewer false positives than rule-based systems. industry data suggests financial institutions deploying machine-learning-based fraud detection see meaningful fraud loss reduction within the first 12 months, with the size of the improvement depending heavily on how mature the prior rule-based system was. As an illustrative example: for a FinTech with $500M in annual payment volume and a current fraud rate of 0.3%, even a 35% reduction in fraud losses equals $525,000 in annual savings — before any operational efficiency gains.

Operational Cost Reduction

The false-positive problem is where operational ROI really compounds. Rule-based systems generate false-positive rates of 90–95%, meaning fraud analysts spend most of their time reviewing legitimate transactions. AI systems reduce false-positive rates to under 10% — meaning the same analyst team can handle 8x the review volume, or you can reduce analyst headcount while maintaining the same coverage. For most mid-size FinTechs, the analyst team cost savings alone justify the AI investment within 18 months.

Revenue Recovery from Reduced False Declines

This is the ROI line that surprises most teams: false declines — legitimate transactions blocked by overly aggressive fraud rules — cost more than the fraud they prevent. industry research consistently shows that false declines cost merchants and FinTechs many times more in lost revenue than the fraud those rules were designed to prevent. AI-powered systems, by accurately distinguishing fraudulent from legitimate transactions, recover that blocked revenue. A FinTech with a 1.5% false-decline rate on $1B annual volume recovers $15M in GMV by halving that rate — representing far more than the cost of the AI system itself.

Chargeback and Dispute Management Savings

Each chargeback costs a FinTech or payment processor an average of $15–50 in direct dispute handling costs, on top of the transaction value. AI systems that prevent fraudulent transactions upstream eliminate the downstream chargeback entirely. For high-volume platforms, reducing chargebacks from 0.8% to 0.2% of transaction volume is worth millions in direct operational savings annually — plus the network penalty avoidance from staying below card network chargeback thresholds.

Implementation Timeline and Break-Even

An AI fraud detection implementation at DreamzTech typically follows a 16-week delivery roadmap: weeks 1-4 for data pipeline and feature store build, weeks 5-10 for model training and validation, weeks 11-14 for decisioning engine integration and UAT, weeks 15-16 for production rollout with shadow mode validation. Break-even on implementation investment, based on the ROI drivers above, typically occurs between months 8 and 14 for mid-market FinTechs — and within months 4-6 for high-volume platforms where the fraud loss numbers are larger. Our AI development services team structures engagements with milestone-based payment to align our incentives with your outcomes.

Figure 6: AI Fraud Detection Software: How FinTech Achieves 99%+ Accuracy in 2026 ROI metrics

Common Pitfalls to Avoid When Deploying AI Fraud Detection

The difference between a successful AI fraud detection deployment and an expensive failed project usually comes down to five avoidable mistakes. We’ve seen all of them — some the hard way.

Pitfall 1: Training on Imbalanced Data Without Correcting for It

Fraud events are rare — typically 0.1–2% of transactions in most FinTech contexts. A model trained on raw transactional data will learn to predict “not fraud” for everything and achieve 99% accuracy on paper while catching zero actual fraud. This is the most common mistake in in-house fraud AI builds. The fix requires deliberate sampling strategies (SMOTE oversampling, undersampling, class weighting) and evaluation metrics that reflect fraud-specific performance: precision-recall AUC and F1-score at the operating threshold, not overall accuracy.

Pitfall 2: Ignoring Model Drift Until It’s a Crisis

A fraud model deployed in January may be significantly degraded by July as fraud patterns shift. Without automated drift monitoring — tracking the distribution of features and score distributions over time, and triggering alerts when they diverge from training baselines — teams only discover model degradation when fraud losses spike on the dashboard. By then, weeks of losses have accumulated. Every production AI fraud system needs automated monitoring with defined drift thresholds and automatic escalation to model retraining.

Pitfall 3: Treating the Fraud System as a Set-and-Forget Black Box

AI fraud models are not fire-and-forget deployments. They require continuous feedback loops: fraud analysts confirming or overturning decisions, chargeback outcomes flowing back into training labels, new fraud vectors being investigated and added to feature sets. Organizations that deploy AI fraud detection and stop investing in the feedback loop see model performance degrade to rule-engine levels within 12-18 months. The model is only as good as the labeled data you keep feeding it.

Pitfall 4: Setting the Wrong Operating Threshold

Every fraud model produces a probability score. The decision of what score threshold to act on — approve, step-up, decline — is a business decision, not a model decision. Setting the threshold too low maximizes fraud catches but destroys legitimate customer approval rates. Setting it too high catches nothing. The right threshold is calibrated to your specific fraud economics: fraud loss per transaction, false-decline revenue loss per transaction, and cost of step-up authentication. This calibration needs to be revisited quarterly and should be done in partnership between your data science team, fraud operations, and finance.

Pitfall 5: Building Without a Regulatory Strategy

Deploying an AI system that makes or informs adverse financial decisions without a regulatory strategy is not just risky — it’s potentially illegal in several major markets. The EU AI Act classifies AI systems making consequential financial decisions as “high-risk” systems subject to mandatory conformity assessments. In the US, the CFPB has issued guidance on AI-driven credit and fraud decisions. Your AI fraud system needs a documented model card, fairness audit, explainability framework, and data governance policy before it goes into production. DreamzTech’s AI consulting team includes regulatory strategy as a standard component of every financial services AI engagement.

Future Trends: What’s Coming in AI Fraud Detection Through 2027

The technology roadmap for AI fraud detection over the next 24 months is moving in three clear directions. Teams building infrastructure today should architect for these capabilities to avoid a painful rebuild cycle in 18 months.

Federated Learning for Cross-Institution Fraud Intelligence

One of the fundamental challenges in fraud detection is that each institution trains on its own fraud data — missing the cross-institution patterns that fraud rings exploit by targeting multiple lenders or payment networks simultaneously. Federated learning enables institutions to collaborate on model training without sharing raw customer data: each institution trains locally, and only encrypted model gradients (not transaction records) are shared to improve a shared global model. Several major banking consortia in Europe and APAC are already running federated fraud intelligence networks. This will become standard practice in FinTech by 2027.

Large Language Models for Fraud Investigation Automation

LLMs are beginning to transform the fraud analyst workbench. Rather than reading raw transaction logs, analysts interact with an LLM-powered interface that summarizes case evidence, generates investigation narratives, suggests next investigative steps, and drafts SAR (Suspicious Activity Report) filings. Early implementations are reducing fraud investigation time per case by 40–60% — dramatically increasing the number of cases a fixed analyst team can handle. The models are trained on historical confirmed fraud cases and SAR filings, not on general internet data.

Real-Time Network Graph Scoring at Scale

Graph neural networks are powerful but computationally expensive — which has historically limited their use in real-time decisioning. New graph database architectures (TigerGraph, Neo4j’s streaming capabilities) combined with purpose-built GNN inference optimization are bringing graph-based fraud scoring into the sub-100ms regime. By 2026, real-time graph scoring will be accessible for mid-market FinTechs that couldn’t previously afford the infrastructure investment, dramatically improving detection of organized fraud rings.

The Bottom Line: Three Things to Take From This Post

AI fraud detection is a large topic. Here’s what matters most if you’re making decisions in the next 90 days:

- Architecture determines outcomes, not marketing claims. The difference between a 94% accurate fraud system and a 99%+ accurate one is in the ensemble design, feature engineering pipeline, and continuous learning infrastructure — not the vendor’s landing page. Demand architectural transparency in every evaluation.

- False declines cost more than fraud in most FinTech contexts. If your fraud team is optimizing only for fraud catch rate, you’re solving half the problem. ROI-maximizing AI fraud systems are calibrated to simultaneously minimize fraud losses and false-decline revenue loss. Both numbers belong in your business case.

- MLOps is the long game. The model you deploy today is not the model that will be running in 18 months — or it shouldn’t be. Invest in the retraining pipeline, monitoring infrastructure, and feedback loop processes from day one, or your fraud detection will degrade as fast as the threat landscape evolves.

Conclusion

The fraudsters are not waiting for your next budget cycle. They’re running automated attacks against your payment stack right now, probing for synthetic identity vulnerabilities, testing behavioral signal gaps, and exploiting the 24-hour lag between a new fraud pattern emerging and your rule engine being updated to catch it. The only architecture that keeps pace is one that learns continuously, scores in real time, and fuses more signal types than any human analyst can process manually.

AI fraud detection software at its best is not a vendor product you plug in — it’s a system of systems: feature engineering pipelines that ingest behavioral and network signals, ensemble models that combine gradient boosting with deep learning and graph intelligence, decisioning engines that translate probabilistic scores into business actions, and MLOps infrastructure that makes the whole stack smarter every time a new fraud case is confirmed. Build or buy that architecture, and 99%+ accuracy at sub-100ms latency is an engineering result, not a marketing claim.

The companies that get this right in 2026 will have a structural cost and trust advantage over their competitors that compounds every year. The ones that don’t will spend that time managing fraud escalations, chargeback disputes, and regulatory inquiries — instead of building their product.

DreamzTech’s AI development team is ready to help you build the right fraud architecture for your platform. Reach out and let’s start with your fraud stack review.

Frequently Asked Questions

1. What accuracy rates can AI fraud detection software realistically achieve?

Enterprise-grade AI fraud detection systems regularly achieve accuracy rates of 99% or higher on production transaction data — but “accuracy” is a misleading metric in fraud contexts because of class imbalance. The more meaningful metrics are precision (of the transactions you flag as fraud, how many actually are fraud), recall (of all actual fraud, what percentage do you catch), and false-positive rate (what percentage of legitimate transactions do you incorrectly block). Leading systems achieve precision rates above 95% and recall above 90% simultaneously, while reducing false-positive rates to under 5%. These figures require ensemble model architectures, comprehensive feature engineering, and continuous retraining — not just off-the-shelf models applied to raw transaction logs.

2. How fast does an AI fraud detection system need to be for real-time payments?

For real-time payment rails (FedNow, Faster Payments, UPI, PIX), the fraud decisioning system must complete scoring and return an approve/decline decision within 100–200 milliseconds of receiving the transaction — because the payment rail itself settles in under 10 seconds and the fraud check happens within that window. Best-in-class implementations achieve p99 scoring latency below 50ms by using pre-computed feature aggregates in low-latency feature stores (Redis), optimized model inference (ONNX Runtime or TensorRT), and horizontally scaled scoring microservices. Any system that requires batch processing or cannot meet sub-100ms latency at peak volume is architecturally incompatible with modern instant payment infrastructure.

3. Should we build AI fraud detection in-house or buy a vendor platform?

The honest answer is: it depends on your data volume, engineering maturity, and differentiation strategy. Vendor platforms (like AWS Fraud Detector, Sardine, or Sift) offer faster time-to-value and proven infrastructure, but typically impose limits on custom model integration, charge per-transaction pricing that scales poorly at high volume, and give you limited visibility into the model internals. Building in-house gives you full control, lower long-run unit economics at scale, and the ability to incorporate proprietary signals unique to your platform — but requires 6–12 months of foundational MLOps investment before you have a production-ready system. A hybrid approach — using a vendor platform for speed while building proprietary model layers on top — is often the right answer for mid-market FinTechs. DreamzTech designs all three approaches and can help you evaluate based on your specific context.

4. What data is needed to train an effective AI fraud detection model?

At minimum, you need 12–24 months of labeled transaction history with confirmed fraud outcomes — meaning transactions that were later confirmed as fraudulent via chargebacks, customer disputes, or investigator confirmation. The more labeled fraud examples you have, the better, but you also need to address class imbalance (fraud events are rare) through sampling strategies. Beyond labeled history, effective models require feature-rich transaction records including device signals, IP/geolocation data, session behavioral data, and account relationship data. If you’re a new FinTech without 12 months of fraud history, transfer learning from pre-trained models or consortium data partnerships can help bridge the cold-start problem.

5. How do AI fraud detection systems handle new fraud patterns they haven’t seen before?

This is the critical limitation of purely supervised approaches — a model trained only on historical fraud labels cannot detect genuinely novel attack patterns. Enterprise fraud systems address this through unsupervised anomaly detection: Isolation Forests, Autoencoders, and statistical process control methods that flag statistically unusual events regardless of whether they match any known fraud pattern. These anomaly signals are fed into the fraud analyst queue for human review, and confirmed cases become new training labels that improve the supervised models. The combination of supervised detection (for known fraud types) and unsupervised anomaly detection (for novel patterns) is what allows AI systems to catch emerging fraud vectors within days rather than after months of rule-writing.

6. What are the regulatory requirements for AI fraud detection in financial services?

Regulatory requirements vary by jurisdiction but converge on several common themes. In the US, ECOA and FCRA require that automated adverse actions (declines, account restrictions) be explainable to the affected customer with specific reasons — which means your AI system must produce per-decision explainability, not just an aggregate model score. The EU AI Act classifies AI systems making consequential financial decisions as “high-risk,” requiring conformity assessments, bias audits, and documentation before deployment. GDPR requires a legal basis for processing personal data in model training, and data subject access requests may require you to explain automated decisions. In the UK, FCA guidance on AI in financial services is increasingly specific about model governance requirements. Your AI fraud system needs a documented model card, fairness testing across protected groups, and a data governance policy before go-live — not as an afterthought.

7. How long does it take to implement AI fraud detection from scratch?

A full-stack AI fraud detection implementation — from data pipeline through production deployment — typically requires 14–20 weeks for a mid-market FinTech platform. The timeline breaks down roughly as follows: 4 weeks for data infrastructure (feature store, streaming pipeline, historical data ingestion), 4–6 weeks for model development and validation, 4 weeks for decisioning engine integration and case management tooling, and 2–4 weeks for shadow-mode validation (running the AI system in parallel with your existing system before full cutover). Shadow-mode validation is non-negotiable — it lets you validate accuracy against real production traffic without any customer impact. Teams that skip shadow mode and deploy directly to production consistently face accuracy surprises that create customer experience incidents.

8. What is the typical ROI timeline for AI fraud detection investment?

Based on published research and DreamzTech’s implementation experience, most FinTechs see positive ROI from AI fraud detection within 8–18 months of deployment, depending on transaction volume and pre-existing fraud rates. The ROI accelerates as the feedback loop matures — the more confirmed fraud cases flow back into retraining, the more accurate the system becomes, compounding both fraud prevention and false-decline recovery simultaneously. High-volume platforms (processing over $1B annually) typically see break-even within 6 months purely on fraud loss reduction. Mid-market platforms (under $500M annually) typically reach break-even at 12–18 months, with the majority of ROI coming from operational cost reduction (analyst efficiency) and recovered false-decline revenue rather than direct fraud loss savings alone.

9. Can AI fraud detection be applied to non-payment fraud — like account takeover or identity fraud?

Absolutely — and in many organizations, account takeover (ATO) and identity fraud represent larger loss vectors than payment fraud. AI-powered ATO detection uses behavioral biometrics (typing cadence, navigation patterns, session behavior) to detect when an account is being accessed by someone other than the legitimate owner, even when the correct credentials are presented. Identity fraud at account opening is addressed through AI-powered document verification, biometric liveness detection, and graph-based synthetic identity detection. The same ensemble model architecture applies across these use cases, though the feature sets and training data differ. A mature AI fraud program typically addresses payment fraud, ATO, identity fraud, and internal fraud (employee misconduct) through a unified feature platform and shared model infrastructure — not separate siloed systems for each fraud type.